Financial Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or legal advice. We are not licensed financial advisors. Always consult a qualified financial professional before making any financial decisions.

myFICO Review

The only place to get your official FICO scores from all three bureaus — what lenders actually see

Last reviewed: 2026-05-25 · By GBBR Editorial Team

Affiliate disclosure: We earn a commission on qualifying purchases. Rankings are never for sale.

Our Top Pick · Gold Tier

myFICO

From $19.95/mo

The Bottom Line

myFICO earns Gold as the definitive credit score monitoring service: it's the consumer arm of Fair Isaac Corporation (FICO), the company that invented credit scoring and whose models are used in 90% of US lending decisions. The difference between myFICO and everything else is simple — myFICO shows you the actual FICO scores your lenders will pull, from all three bureaus, across multiple scoring models (FICO 8, FICO 9, FICO Auto Score, FICO Mortgage Score). Credit Karma shows you VantageScore, which is an estimate. When you're about to apply for a mortgage, car loan, or apartment, myFICO tells you what the lender sees. The $29.95/mo Advanced plan is expensive but fully justified when accuracy matters.

What is myFICO?

myFICO is the consumer division of Fair Isaac Corporation, founded in 1956 and headquartered in Bozeman, Montana. Fair Isaac invented the FICO credit score in 1989, and FICO scores are now used in over 90% of US lending decisions. The myFICO platform was launched to give consumers direct access to the same scores their lenders pull — addressing the widespread frustration of checking a free credit score tool and seeing a different number than what a lender reports during an application. myFICO holds unique authority as the originator of the scoring model.

What does myFICO offer?

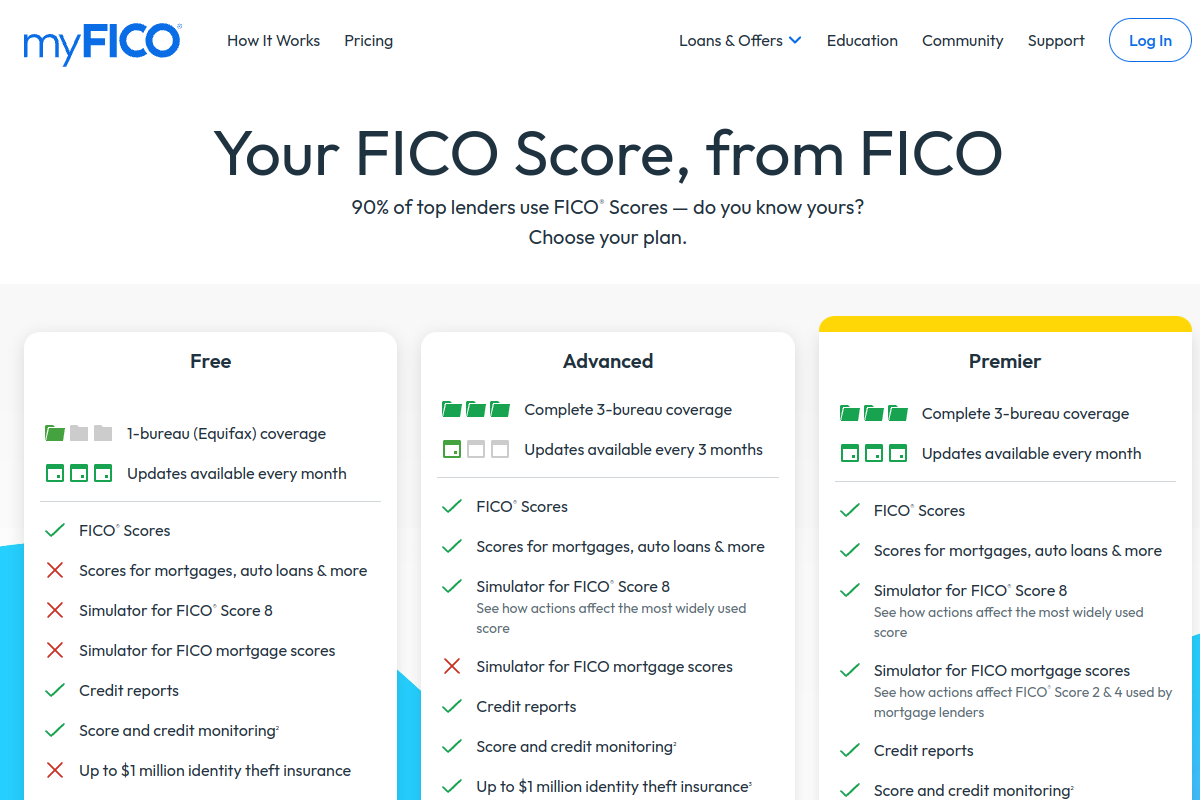

myFICO Basic ($19.95/mo) provides FICO Score 8 from one bureau with monthly updates. myFICO Advanced ($29.95/mo) gives FICO scores from all three bureaus (Equifax, TransUnion, Experian) updated quarterly, with 3-bureau credit monitoring and identity protection features. myFICO Premier ($39.95/mo) upgrades to monthly 3-bureau score updates plus enhanced identity theft insurance. One-time credit reports are also available. The 3-bureau product subscription earns the $100 affiliate commission. myFICO Score Simulator shows how credit actions would affect your scores.

Basic (1 bureau)

$19.95

/month

Advanced (3 bureaus, quarterly)

$29.95

/month

Premier (3 bureaus, monthly)

$39.95

/month

Is myFICO worth the price?

Expensive for ongoing monitoring, but justified when you actually need the lender-accurate scores — essential before any major loan application

myFICO Advanced at $29.95/mo shows FICO 8 + FICO Auto + FICO Mortgage scores from all 3 bureaus — Credit Karma shows VantageScore that may vary 20–100 points from what your lender sees

Premium price for genuine accuracyHow we scored it

Overall score: 85/100

Official FICO scores from all 3 bureaus — FICO 8, FICO 9, FICO Auto Score, FICO Mortgage Score. The same models your lenders use.

3-bureau monitoring with alerts for new accounts, hard inquiries, address changes, and identity threats on Advanced and Premier plans

Score Simulator shows how actions affect scores; educational resources on what drives FICO scores; no active dispute services — monitoring only

No free tier — paid subscription required starting at $19.95/mo

$29.95/mo Advanced is expensive for passive monitoring but justified before major loan applications

Phone and email support; strong educational resources about FICO scoring; no active repair services

Why myFICO is Gold Tier

myFICO earns Gold for being the only source of genuine multi-bureau FICO scores for consumers. The distinction between FICO and VantageScore is not marketing — it's the difference between knowing your credit standing and guessing it. For anyone preparing for a major purchase (home, car, business loan), myFICO's score accuracy is invaluable. The monthly cost is high for passive monitoring, which is the main trade-off vs. free options.

Pros & Cons

Pros

- Official FICO scores from all 3 bureaus — the exact scores your lenders see

- Multiple FICO models: FICO 8, FICO 9, FICO Auto Score, FICO Mortgage Score

- Score Simulator: shows how credit actions would impact your scores

- 60-day cookie window for affiliates — $100 CPA on 3-bureau annual subscription

- Identity theft insurance on Advanced and Premier plans

Cons

- No free tier — requires paid subscription

- $29.95/mo Advanced is expensive for ongoing monitoring

- No active dispute or repair services — monitoring only

Ready to try myFICO? Plans start at $19.95/mo.

Get myFICO — from $19.95/mo →Frequently Asked Questions

Is myFICO worth it in 2026?

Expensive for ongoing monitoring, but justified when you actually need the lender-accurate scores — essential before any major loan application Overall verdict: Premium price for genuine accuracy.

What is myFICO best for?

myFICO is best for: Anyone preparing to apply for a mortgage, car loan, or apartment in the next 6 months, People who have seen a mismatch between their 'free' credit score and what a lender reported, Credit-conscious consumers who want the authoritative score, not an approximation.

Does myFICO have a free trial?

myFICO does not offer a permanently free plan. Paid plans start at $19.95/month.

Who should NOT use myFICO?

myFICO is not the right fit for: Passive ongoing monitoring where free options are sufficient (use Experian free); People who need active dispute/repair services (use Sky Blue or Lexington Law).

What are the best myFICO alternatives?

Top alternatives to myFICO include experian, credit-karma, sky-blue-credit.

myFICO earns Gold for being the only source of genuine multi-bureau FICO scores for consumers. The distinction between FICO and VantageScore is not marketing — it's the difference between knowing your credit standing and guessing it. For anyone preparing for a major purchase (home, car, business loan), myFICO's score accuracy is invaluable. The monthly cost is high for passive monitoring, which is the main trade-off vs. free options.

Get myFICO →Community Reviews

Loading reviews...